Statutory Health Insurance (GKV)

Overview

In Germany, ~75 million people or 90% of the country’s population is covered by statutory health insurance providers. There are 93 of them as of January, 2026. Any one who is living in Germany needs to have health insurance as well as long-term care insurance. You sign up for both health and long-term care insurance with the same provider. The statutory health insurance is a solidarity system, where your health insurance contributions depend on your income. The private health insurance, on the other hand, works on the equivalency principle in which the contributions depend on age and the type of cover you choose. Not every one can opt for private health insurance since it has certain eligibility criteria.

The statutory health insurance providers are public-law corporations which means that they are public, non-profit bodies with elected self-governance. The fundamental principles of statutory health insurance are the solidarity principle and the principle of benefits in kind. The solidarity principle guarantees that each insured person receives the medically-necessary benefits from the health insurance, regardless of their income or of the amount of premiums which they have paid. The principles of benefits in kind ensures benefits without up-front payments on the part of the insured.

Monthly Contributions in GKV

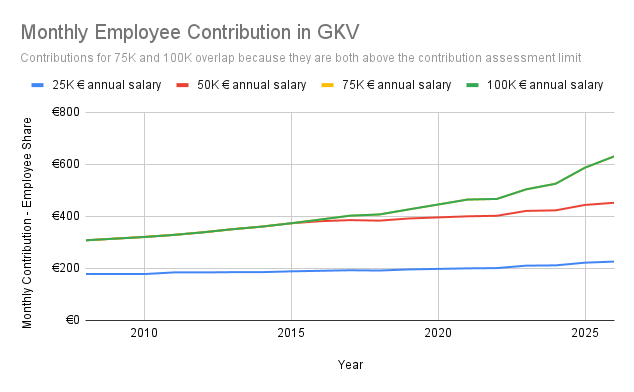

Each statutory health insurance provider charges a general contribution and an additional contribution. The monthly general contribution rate is 14.6% by law across all providers. However, the monthly additional contribution rate varies across providers, the national average in 2026 being ~2.9%. The insurance contribution has a contribution assessment limit, which in 2026 is €5,812.50. What this means is that if your gross monthly salary is more than this limit, then the insurance contribution will be calculated on this amount and the employer is required to pay 50% of these contributions. For gross salary below this limit, you will pay half of ~17.1% of your monthly gross salary as your health & long-term care insurance contribution. Your employer will pay the other half. If you are self-employed, you pay the entire contribution yourself. Here’s a chart showing how the monthly contributions for GKV differ for different wage levels.

Data Source: GKV Spitzenverband, Sozialpolitik aktuell

Data Source: GKV Spitzenverband, Sozialpolitik aktuell

Services in GKV

The services to be provided by statutory health insurance providers are legally defined by law i.e. SGB V. What separates these companies is the quality of service and the extras. Extras includes things such as travel vaccinations, precautionary checks and bonus programs. Your choice will ultimately depend on what you value the most. We recommend to calculate your monthly insurance contributions for your salary with different providers and see whether it makes a tangible difference for you. If you are moving to Germany and are especially interested in English-speaking support, some GKV providers such as TK and Barmer are good in providing support in English. Here is a list of all statutory health insurance companies in Germany. In case you are not happy with the choice of your statutory health insurance provider, you always have the possibility to change to a different provider. You also have the option of choosing add-on tariffs on top of your statutory health insurance. These add-ons give you extra services on top of what is covered by statutory health insurance such as your own room during a hospital stay, the option to see a chief physician, certain dental treatments etc.

KVdR

KVdR (Krankenversicherung der Rentner) is the health insurance status for pensioners, which has certain advantages. With the KVdR status, the pensioner only pays monthly contributions on statutory & company pensions and their work income. They don’t pay contributions on other sources of income - rent, interest, dividends and private pension plans. Without the KVdR status, they need to pay contributions on all income sources.

Qualifying for KVdR

To qualify for the KVdR status, you need to meet two criteria.

- Pre-insurance period: One needs to be insured in the statutory health insurance system for at least 90% of the time during the second half of their working life. It doesn’t matter how you are insured in the statutory system - compulsorily insured, voluntarily insured or through family insurance. For each child that you have, you get 3 years added as a benefit towards your pre-insurance period.

- You must be eligible for statutory pension, for which you must have contributed towards the statutory pension system in Germany for at least 5 years.

Was this helpful?

Your feedback helps us improve our guides