Going freelance in Germany - what happens to your health insurance?

You are a salaried employee working in Germany and have decided to fulfill your dream of being an entrepreneur or a freelancer. As you take this exciting step, what happens to your health insurance? As a salaried employee, you might be insured in statutory health insurance (GKV) or private health insurance (PKV). Your employer would have been paying 50% of your health insurance contributions, up to a maximum of 50% of the contribution assessment limit (2026: 69,750 euros per year, 5,812.50 euros per month). Once you go freelance and become your own boss, you lose this employer contribution share and pay the entire premium yourself.

Going self-employed as a GKV salaried employee

As a salaried employee in statutory health insurance (GKV), you could either be compulsorily or voluntarily insured. Your income level determines this distinction. If you are earning below the JAEG (Jahresarbeitsentgeltgrenze), you need to be compulsorily insured in the statutory system and can’t opt for private health insurance. If you earn above the JAEG, you can either be voluntarily insured in the statutory system or choose private health insurance. Once you become a freelancer, you can either continue to be insured in GKV as a voluntary member or switch to private health insurance (PKV). The JAEG criteria doesn’t apply for a self-employed person.

In GKV, the contributions are calculated as a percentage of the salary. A GKV member must pay - 14.6% as the general contribution rate and 2.9% as the additional contribution rate (varies by provider) towards their health insurance. For the long-term care insurance, one must pay 3.6% (4.2% if they are childless and over 23). As a salaried employee, you only pay roughly half of these contributions. The employer pays the other half. As an example, if you were earning €10,000 per month, your total monthly contribution towards health and long-term care insurance would be €1017.19 and €209.25 respectively. The employer would pay half of the health insurance premium and slightly less than half of the long-term care insurance premium. As a freelancer, you lose the employer share and pay the entire contribution yourself.

Many freelancers are surprised when they find out that they need to consider all income types to calculate their monthly contribution – freelance income, investment income, rental income, dividend income and so on. The monthly contribution amount has a minimum and a maximum assessment base. In 2026, the minimum assessment base is €1318.33 per month and the maximum assessment base is €5812.50 per month. These serve as the lower and upper thresholds respectively for calculating the monthly contributions for health and long-term care insurance.

Going self-employed as a PKV salaried employee

If you are a salaried employee with private health insurance (PKV) about to become self-employed, the only change in your health insurance would be that you pay the entire monthly premium yourself and lose the employer share. In this case, you have the possibility of moving to a cheaper tariff with your health insurance provider to save on costs. However, you should make such a change with caution. By moving to a cheaper tariff, you might lose coverage for certain health benefits and might only get them back later by undergoing a health check.

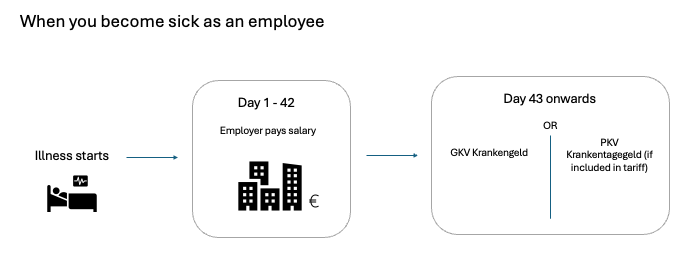

The biggest self-employed dilemma – Income loss when you become ill

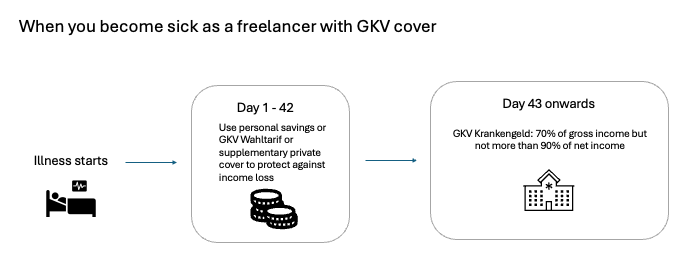

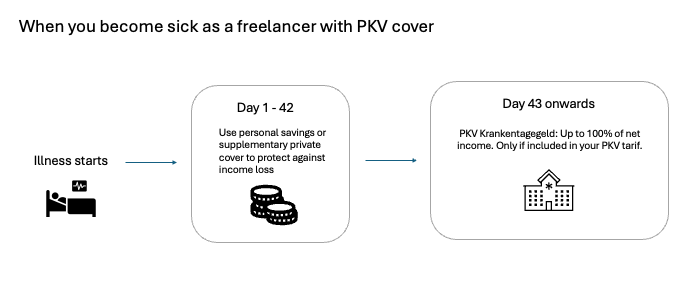

Irrespective of whether you are in GKV or PKV as a salaried employee, your employer pays your salary for 6 weeks (42 days) once you become ill. Once you become a freelancer, you no longer have this 6-weeks income protection. You could either rely on your savings, consider a supplementary private insurance or a GKV Wahltarif to protect against this income loss.

For a freelancer with GKV cover:

A freelancer who is voluntarily insured in GKV, has the option of paying the general contribution rate of 14.6% or a reduced rate of 14%. If they pay 14.6%, they would have access to the Krankengeld benefit from day 43 onwards. If they pay 14%, they lose access to this benefit. In both cases, they need to deal with the income loss during days 1 – 42.

The amount of Krankengeld benefit in GKV is calculated as 70% of the gross income but it can’t exceed the 90% of the net income. Your GKV provider would pay you this amount for a maximum of 78 weeks. The Krankengeld benefit generally starts from day 43 but can start earlier (day 15 or 22) with the GKV Wahltarif.

For a freelancer with PKV cover:

From day 43 onwards of being ill, your private health insurance provider would pay Krankentagegeld benefit, if you have opted in for this benefit in your tariff. This is not always a default option in PKV. So, it is recommended to check your tariff details, if you are unsure. You have the option of receiving this benefit earlier than day 43 by choosing the appropriate tarif option.

The amount of Krankentagegeld is capped at 100% of your net income. PKV providers pay this benefit while you are temporarily unable to work (arbeitsunfähig); they stop paying this benefit once you are classified as permanently occupationally disabled (berufsunfähig).

Employee to Freelancer - what concrete steps do you need to take for health insurance?

You can be either voluntarily insured in GKV or privately insured in PKV. Both are good paths. The choice depends on your personal situation. For a freelancer with a spouse and children, being privately insured would mean a separate health insurance contract for each family member. In the statutory health insurance, the child and the non-working spouse can be insured for free in the family insurance. Making a switch to private health insurance might save you money in the short-term but you also need to evaluate the situation over the longer term. You can compare your lifetime GKV vs PKV costs with our calculator.

The most important thing that requires attention is how you would cover your income loss, if you become ill. Having enough savings or a supplementary private cover can provide you that sense of security as you embark on the uncertain and exciting journey of freelancing.

Checklist – Going self-employed as a GKV insured employee

1. Inform your Krankenkasse of your status change from employee to a freelancer.

2. Your Krankenkasse would ask you for an income estimate. Your monthly contributions are set provisionally and corrected retroactively against your Steuerbescheid. So, a low estimate now can mean a back payment later.

3. Decide between 14% and 14.6% for the general contribution rate.

4. Check how you would cover an income loss, if you become ill.

5. If considering a switch to PKV, run the lifetime calculator and get a risk pre-assessment before leaving GKV.

6. If you are becoming a freelancer in the creative profession, check if you are eligible for Künstlersozialkasse (KSK). KSK effectively pays the employer half of the contributions for its members.

Checklist – Going self-employed as a PKV insured employee

1. Check how you would cover an income loss, if you become ill.

2. Check if it makes sense to switch to a cheaper tariff with your PKV provider. Consider using expert advice if you are considering this change.

3. Switching to GKV as a freelancer might not be possible. If you are considering this option, check your eligibility.

This article is meant to be for general information only. Discuss your specific situation with us for advice tailored to your situation.

Want to discuss your situation with us? Book a free 15-minute call.